S&P500 Trading Update 23/4/26

S&P500 Trading Update 23/4/26

***QUOTING ES1! FOR CASH US500 EQUIVALENT LEVELS, SUBTRACT POINT DIFFERENCE***

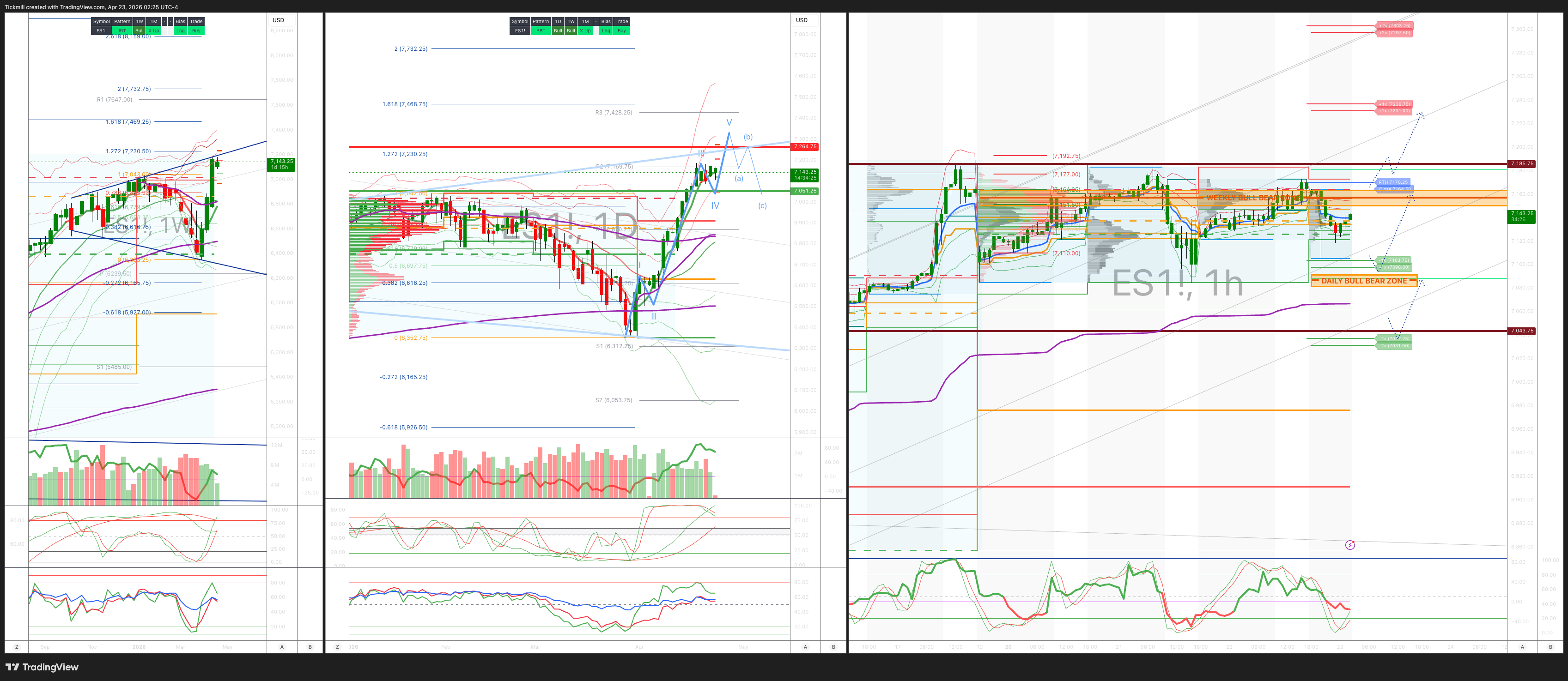

WEEKLY BULL BEAR ZONE 67150/60

WEEKLY RANGE RES 7262 SUP 7050

May OPEX Straddle: 225pt range implies a OPEX to OPEX range of [6900, 7350]

June QOPEX Straddle is 546.4pt giving us a range of [5960,7052]

JHEQX Q2 Collar 6189/6290 - 6865/6955

DEC2025 OPEX to DEC2026 OPEX is 945 points giving us a range of [5889,7779]

SPX PUT/CALL RATIO 1.15 (The numbers reflect options traded during the current session. A put-call ratio below 0.7 is generally considered bullish, and a put-call ratio above 1.0 is generally considered bearish)

DAILY VWAP BULLISH 7130

WEEKLY VWAP BULLISH 6825

MONTHLY VWAP BULLISH 6815

DAILY STRUCTURE – BALANCE - 7185/7085

WEEKLY STRUCTURE – OTFH - 6826

MONTHLY STRUCTURE - OTFD - BALANCE

Balance: This refers to a market condition where prices move within a defined range, reflecting uncertainty as participants await further market-generated information. Our approach to balance includes favouring fade trades at the range extremes (highs/lows) while preparing for potential breakout scenarios if the balance shifts.

One-Time Framing Higher (OTFH): This represents a market trend where each successive bar forms a higher low, signalling a strong and consistent upward movement.

One-Time Framing Down (OTFD): This describes a market trend where each successive bar forms a lower high, indicating a pronounced and steady downward movement.

DAILY BULL BEAR ZONE 7060/50

DELTA FLIP 6831

DAILY RANGE RES 7236 SUP 7103

2 SIGMA RES 7303 SUP 7037

VIX BULL BEAR ZONE 19.5

TRADES & TARGETS

LONG ON REJECT/RECLAIM OF DAILY BULL BEAR ZONE TARGET RTH/ETH CLOSES > DAILY RANGE RES

***ADDITIONAL SETUPS & TARGETS HIGHLIGHTED ON THE CHARTS***

(I FADE TESTS OF 2 SIGMA LEVELS ESPECIALLY INTO THE FINAL HOUR OF THE NY CASH SESSION AS 90% OF THE TIME WHEN TESTED THE MARKET WILL CLOSE ABOVE OR BELOW THESE LEVELS)

GOLDMAN SACHS TRADING DESK VIEW - ‘COMPLACENT’

US equities finished strongly higher on Wednesday, led by Tech and other higher-beta pockets, as investors increasingly looked through geopolitical noise and positioned for a supportive earnings setup. The S&P 500 rose 1.05% to 7,138 with a healthy $3.4bn MOC imbalance to buy, while the Nasdaq 100 outperformed sharply, +1.73% to 26,937. The Russell 2000 gained 0.74% and the Dow added 0.69%. Trading volumes were relatively light at 16bn shares versus a 19.4bn YTD daily average, while VIX fell 3.13% to 18.89, underscoring the market’s willingness to fade Middle East risk headlines even with visibility on Iran negotiations still limited. Trump’s decision to extend the ceasefire indefinitely while keeping the blockade in place helped stabilize sentiment, but the tone still felt somewhat complacent given the lack of hard information on the diplomatic path.

The day’s leadership was very much in the speculative and growth-heavy parts of the tape. Bitcoin, quantum, meme stocks and the “most short” basket all rose 2–5%, reinforcing the sense that investors were willing to reengage with risk rather than hide in defensives. Software remained a key focus, with the beaten-up group now up eight straight sessions, helped by idiosyncratic support from names such as MANH, TWLO, and ADBE. Notably, there is growing investor discomfort with this move after earlier dismissiveness, suggesting the rally is beginning to pressure underweights and shorts. On the desk, overall activity levels were only moderate, but the floor still finished +8% to buy, well above its 30-day average. Asset managers were net buyers of macro products and selective Tech, while hedge funds continued pressing macro shorts, with no major sector skew standing out.

In derivatives, the session reflected headline fatigue and earnings optimism, with QQQ leading in both spot and vol outperformance. Nasdaq vol was bid across the curve, especially in the front end, while SPY and IWM vols were offered. Skew eased across the board after SPX 1m skew had pushed to the 96th percentile on a one-year lookback the day before. Flow-wise, the desk saw a large buyer of short-dated SPX upside and a sizable outright buyer of VIX August topside, while single-name activity in financials and tech was skewed to upside participation. Into the rest of the week, the implied move is a relatively contained 0.83%, with post-close focus shifting to SK Hynix as an important read-across for semis and memory.

Post-bell earnings were broadly constructive for cyclicals and hardware-linked tech. Texas Instruments rose 7% after a clear beat on revenue and EPS and stronger-than-expected guidance. Lam Research added 3% to a solid quarter, with guidance roughly 10% above Street. Tesla gained 3.5%, with investors encouraged by the gross margin and free cash flow upside, even as attention remains on the robotaxi and the “Terafaband” commentary. On the downside, ServiceNow fell 13% as guidance and margin dynamics disappointed, despite a slight beat, while IBM lost 6% after failing to provide a fresh AI backlog figure and simply reiterating full-year guidance. Elsewhere, Molina Healthcare rose 2.5% on favorable medical cost commentary; Medpace fell 17% on weak bookings, Southwest dropped 7% on softer Q2 EPS guidance, and CSX climbed 5% after an earnings beat and supportive medium-term margin framing.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 71% and 74% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!